The US dollar has long been seen as the world’s ultimate safe haven, a currency investors rush toward in times of uncertainty. However, a recent report by ING suggests that while the dollar has lost part of its traditional safe haven appeal since 2024, it has not completely surrendered its global dominance. For anyone wondering whether the world is moving away from the US dollar, the answer, at least for now, appears to be more nuanced than dramatic headlines might suggest.

Last year marked a particularly difficult period for the greenback. The dollar index, which measures the US currency against a basket of major global currencies, fell by nearly 10 percent, making it the weakest annual performance since 2017. Several factors contributed to this slide. Unpredictable trade policies from the United States, tariff threats directed at both rivals and allies, and public criticism of the Federal Reserve by President Donald Trump all created uncertainty in financial markets. When investors sense political or policy instability, confidence in a currency can weaken, and that is exactly what happened.

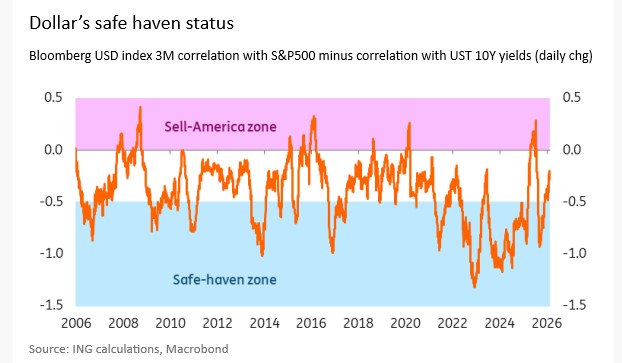

According to ING’s analysis, one way to understand the dollar’s changing role is by looking at how it moves in relation to US stocks and 10-year Treasury bonds over a three-month period. In 2024, the dollar’s safe-haven behavior was stronger, meaning investors tended to move into the currency during times of stress. That protective quality has since diminished to some extent. However, this does not mean that global investors are abandoning the US currency altogether. In fact, private investors still hold more than 80 percent of foreign-owned US assets, and there is no broad evidence of capital flight.

Another key point from the report is that the current weakness in the dollar appears to be cyclical rather than structural. In simple terms, cyclical weakness means the currency is going through a phase that is tied to economic conditions and market cycles, not a fundamental or permanent decline in its global role. Structural weakness, on the other hand, would suggest more serious and longer-lasting damage. For now, ING does not see signs of that kind of shift.

See Related: Tesla Gains Boosted Wall Street’s Main Stock Indexes. Interest Rates Outlook And Job Report Remain In Focus

Reliance On The US currency

There is also little evidence of rapid de-dollarisation. Despite ongoing discussions in global politics about reducing reliance on the US currency, the dollar continues to dominate international assets, liabilities, financial market turnover, and global transactions. Its share in global finance remains significant, and no sharp acceleration away from the dollar has been observed.

One area that remains critical, however, is the independence of the Federal Reserve. The credibility of the US central bank is widely viewed as a cornerstone of global financial stability. If markets were to believe that interest rate cuts were being made for political reasons rather than economic necessity, confidence in the dollar could suffer significantly. In an extreme scenario, this could even trigger a run on the currency, where investors rush to sell dollars out of fear. While that situation is not currently unfolding, it highlights how important central bank independence is for maintaining trust in the financial system.

Looking ahead, ING does not expect this year’s dollar decline to be as severe as last year’s drop. The bank forecasts that the euro could end the year around 1.22 dollars, compared to current levels near 1.18. This suggests continued, but moderate, pressure on the US currency rather than a dramatic collapse.

In summary, while the US dollar has lost part of its safe haven shine, it remains deeply embedded in the global financial system. The recent weakness appears to reflect economic cycles and policy uncertainty rather than a fundamental breakdown in demand. For investors and policymakers alike, the message is clear: the dollar may be under pressure, but it is far from losing its central role in the world economy.